Medicare supplement insurance (Medigap) helps pay some out‑of‑pocket costs that come with Original Medicare.

After discovering there are many financial “gaps” and no “out of pocket maximum” limit to what you could have to pay while only in original Medicare Parts A and B, most people look for a remedy. There are 2 options to fill the “gap”, Option 1 is to add a Medicare Supplement plan and/or a Part D prescription drug plan. Both are offered by private insurance companies. Option 2 is to choose a Medicare Advantage plan to provide all of what Parts A and B would, plus additional benefits. Both options 1 or 2 meet the need but in very different ways.

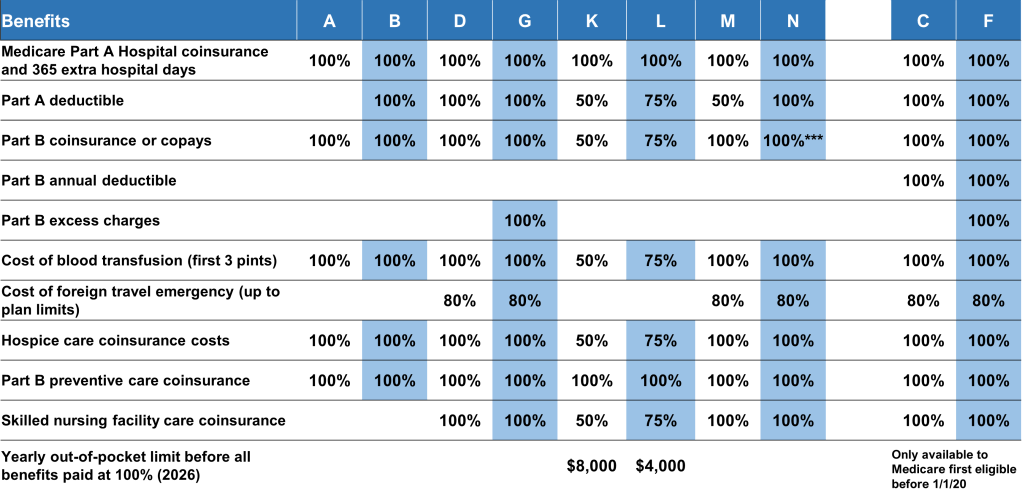

Medicare supplement insurance plans are standardized by the federal government. Each is labeled with a letter. Every plan with the same letter offers the same benefits, no matter what state it’s offered in or by which insurance company.

The level of coverage varies. There are standardized plans that cover all of your Medicare deductibles, copayments and coinsurance, while others leave some costs for you to pay on your own.

You must be enrolled in both Part A and Part B to be eligible for a Medicare Supplement Plan.

For a more in-depth look at how Medicare Supplement Plans work please watch our video

Medicare Supplement Insurance Costs

- Medicare Supplement Insurance Costs, or “Premium”

- Insurance company premiums vary from insurer to insurer even if the plans offer the exact same coverage

- Letter plans that provide more coverage generally have higher premiums.

- Premiums often change from year to year.

Key reasons for considering a Medicare Supplement instead of a Medicare Advantage plan

- Nationwide coverage – You can go to any doctor, anywhere in the U.S. that accepts Medicare coverage

- Managing your costs – the more expensive monthly premium can be a way to manage your health care costs if the plan you choose helps to pay for nearly all of your services, especially if you have regular and frequent doctor visits and services.

Considerations that might not make a Medicare Supplement a good fit for you compared to a Medicare Advantage plan

- Doesn’t include prescription drug coverage so a separate plan and premium will be needed.

- If you don’t require medical service often, the monthly plan premium could be more than you would spend on co-pays, deductibles and total out-of-pocket costs in a Medicare Advantage plan.

- Other costs are required if you add other coverage/services such as Dental, Vision, Hearing, gym membership

- Your coverage has multiple plans – Original Medicare, Med-Sup and a Part D Plan. For some this is an inconvenience.

Remember Medicare supplement plans only fill in the gaps for what Original Medicare does not pay for. If Original Medicare does not cover a specific service neither will a Medicare Supplement Plan.

Medicare Supplement Insurance – How it works.

Medicare supplement insurance pays after Medicare first pays its share. When you go to your doctor for treatment, the office bills Medicare. Medicare processes the bill, and if it approves the service, it pays what it’s supposed to. It then sends the remainder of the charges to your Med Sup plan. The insurance company process the bill and pays its share. Then depending on your plan if there is remaining amount, it is passed on to you. It’s important to understand that Medicare decides if the claim is paid. If Medicare approves the bill your Med Sup plan must pay its share of your deductibles, co-pays, and coinsurance.